Planning ahead for your finances can save you stress down the road, and ensure the success of your personal and professional goals. Outlining a monthly budget is one of the most effective ways to both organize your finances and chart your progress. The following guideline offers some helpful suggestions to stay organized and motivated as you chart your financial future.

The Importance of Setting Up a Budget

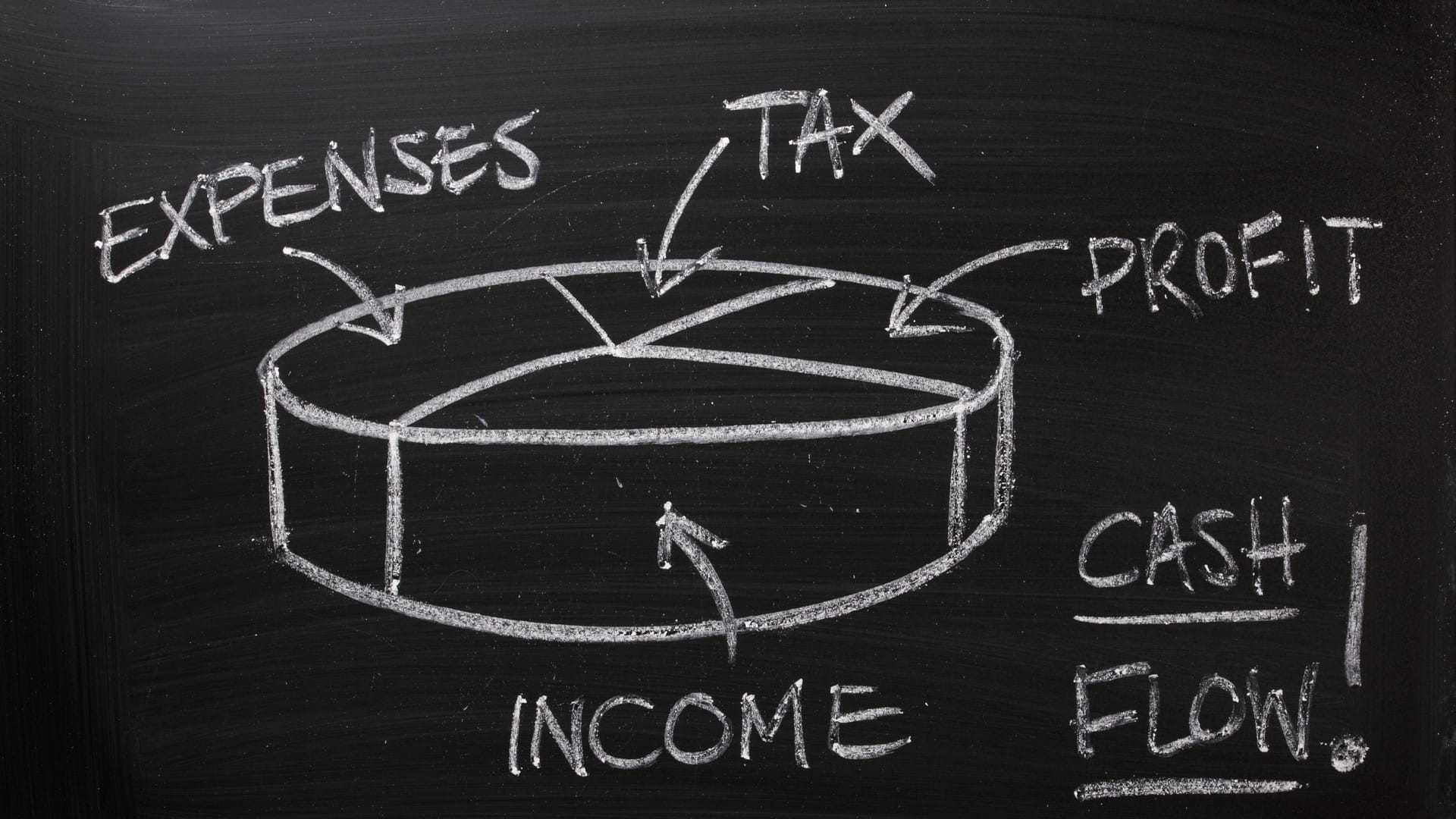

Assessing the amount of money you earn every month after taxes is the first step toward setting up a reliable budget. Next, you should determine how much is needed to satisfy monthly bills and necessary living expenses. Setting up a budget will go a long way toward helping you accomplish your financial goals as you streamline purchases.

Splitting your monthly income into three categories is a popular budgeting method. Under this system, half goes toward absolutely necessary expenses like housing, transportation, utilities, and food, 20% covers retirement and debts, and the last 30% is spent on personal expenses, such as entertainment, personal care, or charity, to name a few examples. As far as personal purchases are concerned, you should really weigh the overall value of what you’re spending money on. Is the purchase an impulse? Does it benefit your daily life in any way beyond instead gratification? One popular sentiment many apply to their spending habits is the idea that memories are more valuable than individual material goods.

The Big (and Small) Picture

As you establish your financial goals, it’s helpful to organize a plan that addresses each goal in smaller, bite-sized installments. We can easily overwhelm ourselves with long-term goals, so assessing what can be realistically accomplished within the near future may ensure long-term success.

Along with drawing up a budget, creating a financial calendar will help organize your tax schedule, whether you have upcoming appointments or need to remind yourself to pay quarterly taxes on time. This visualization can also help you track long term goals through smaller, more immediately achievable tasks, while also allowing you to track your current status. Knowing where you stand will help you stay current on financial goals. Tracking your net worth can also prevent the resumption of bad spending habits and stop current ones in their tracks.

Making the Most of that 20%

The simple act of listing your debts will help you form a plan of attack. Focusing on interest rates instead of what you owe will allow you to effectively prioritize the payoff of individual debts. The bill with the highest interest rate is costing you the most money, so it should take top priority on your list. Once that debt is paid, apply the same method to the next item.